14.08.2024

HHLA increases revenue and benefits from European network expansion

- HHLA’s CEO, Angela Titzrath: “We remain committed to developing HHLA into a leading provider of sustainable, digitalised and networked logistics solutions in Europe.”

- Container handling increased by 2.2 percent to 2,940 thousand TEU (previous year: 2,876 thousand TEU)

- Container transport increased by 1.8 percent to 833 thousand TEU (previous year: 819 thousand TEU)

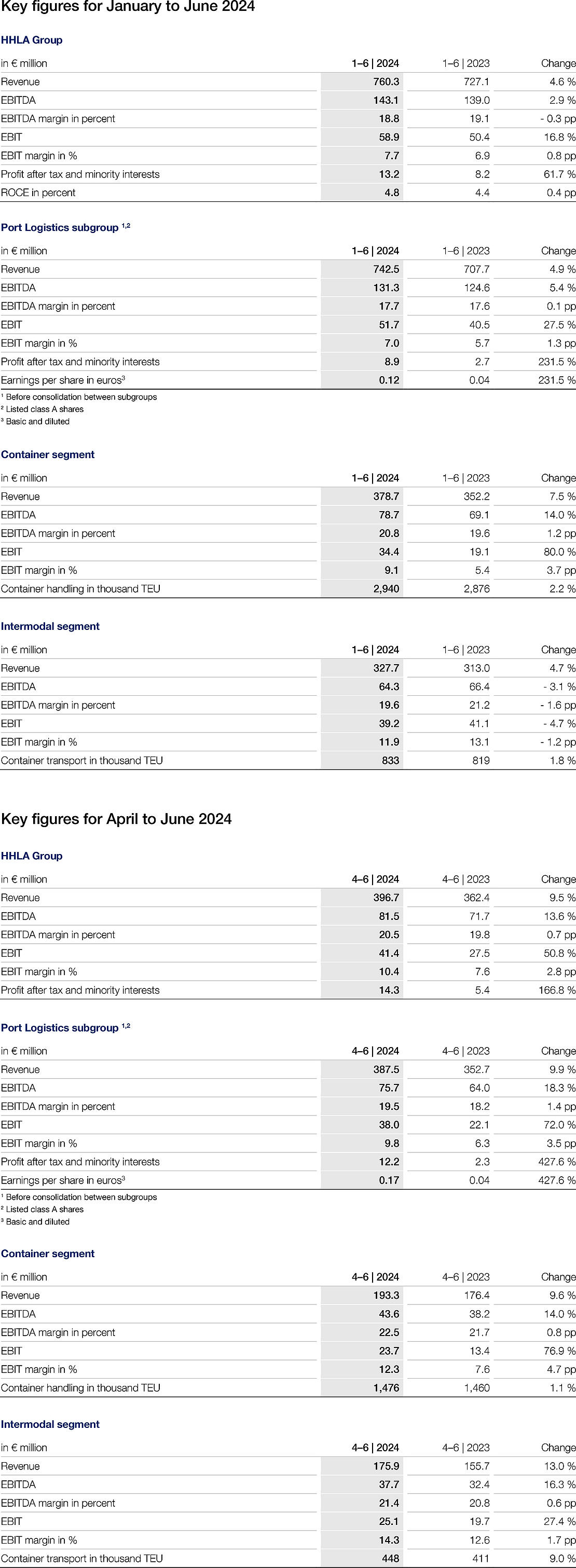

- Group revenue came to € 760.3 million (previous year: € 727.1 million)

After a weak start to the year due to a challenging environment, Hamburger Hafen und Logistik AG (HHLA) concluded the first half of 2024 with positive figures for both revenue and earnings. In addition to rises in container handling and container transport, an advantageous revenue mix and the expansion of the European network also had a beneficial effect. Group revenue rose by 4.6 percent to € 760.3 million (previous year: € 727.1 million). The Group operating result (EBIT) climbed by 16.8 percent to € 58.9 million (previous year: € 50.4 million). The EBIT margin amounted to 7.7 percent (previous year: 6.9 percent). Consolidated profit after tax and minority interests came to € 13.2 million (previous year: € 8.2 million).

Angela Titzrath, Chief Executive Officer of HHLA: “The first half of the year was characterised by a challenging market environment for HHLA. Despite making the necessary adjustments due to supply chain disruptions, HHLA was still able to achieve growth in container handling and transport. Even if the business forecast remains challenging due to the weak economy, ongoing crises and changes in the market, HHLA is in a strong position thanks to its strategic approach. We are therefore continuing to invest in our European network, the modernisation of our terminals, the qualification of our employees and the development of sustainable logistics solutions.”

Port Logistics subgroup: performance January – June 2024

The listed Port Logistics subgroup recorded a moderate increase in revenue to € 742.5 million in the first six months (previous year: € 707.7 million). The operating result (EBIT) increased by 27.5 percent to € 51.7 million (previous year: € 40.5 million), while the EBIT margin rose year-on-year by 1.3 percentage points to 7.0 percent. Profit after tax and minority interests came to € 8.9 million (previous year: € 2.7 million). Earnings per share thus amounted to € 0.12 (previous year: € 0.04).

In the Container segment, container throughput at HHLA’s container terminals rose by 2.2 percent compared to the weak prior-year figure to 2,940 thousand standard containers (TEU) in the first half of 2024 (previous year: 2,876 thousand TEU). At 2,811 thousand TEU, handling volume at the Hamburg container terminals was up 1.7 percent on the same period of the previous year (previous year: 2,763 thousand TEU). In terms of overseas traffic, this positive volume trend was primarily due to, on the one hand, the North, South and Central America shipping regions, with cargo volumes in the United States recording a particularly substantial increase. On the other hand, a positive trend was witnessed in the cargo volumes with other European seaports in light of temporary route adjustments due to the military conflict in the Red Sea. Handling volumes in the Far and Middle East shipping regions, however, moderately declined. Feeder traffic volumes were moderately up on the previous year. The proportion of seaborne handling by feeders stood at 18.7 percent (previous year: 18.4 percent).

The international container terminals reported a rise in handling volume of 13.5 percent to 129 thousand TEU (previous year: 113 thousand TEU), driven by the strong growth at the multi-function terminal HHLA TK Estonia. This more than compensated for the reduction in handling volume at HHLA PLT Italy in Trieste due to blank sailings and ships being rerouted as a consequence of the military conflict in the Red Sea. Seaborne handling at Container Terminal Odessa (CTO) remained suspended by the authorities in the first half of the year due to the Russian invasion.

Segment revenue rose significantly by 7.5 percent in the reporting period to € 378.7 million (previous year: € 352.2 million). This was mainly due to longer dwell times for containers handled at the Hamburg container terminals compared to the previous year and the resulting rise in storage charges. In addition, the positive trend at HHLA’s international container terminals contributed to the increase in revenue. Alongside earnings from handling-related activities at CTO, positive volume growth at the HHLA TK Estonia terminal in Tallinn, as well as higher earnings at the multi-function terminal in Trieste, had a positive effect.

The operating result (EBIT) rose by 80.0 percent to € 34.4 million in the reporting period (previous year: € 19.1 million), mainly due to the improved revenue trend. The operative cost increases in the first six months were offset to a large degree through measures to safeguard earnings. The EBIT margin increased by 3.7 percentage points to 9.1 percent (previous year: 5.4 percent).

The Intermodal segment saw a slight increase in volumes in the first half of 2024. Container transport increased by a total of 1.8 percent to 833 thousand TEU overall (previous year: 819 thousand TEU).

Rail transport rose by 4.0 percent year-on-year to 719 thousand TEU (previous year: 691 thousand TEU). Here, the sharp rise in transport volumes in the German speaking region more than compensated for the decline in traffic with Adriatic seaports and the decline in Polish traffic. The acquisition of a majority shareholding in Roland Spedition GmbH in the second quarter also contributed to the rise. There was a strong decrease of 10.0 percent in road transport to 115 thousand TEU (previous year: 128 thousand TEU).

With year-on-year growth of 4.7 percent to € 327.7 million (previous year: € 313.0 million), revenue growth was stronger than the increase in transport volumes. Alongside routine price adjustments, this was due to the higher share of rail traffic in transport volumes, which was up 1.8 percentage points year-on-year at 86.2 percent (previous year: 84.4 percent).

The operating result (EBIT) decreased by 4.7 percent to € 39.2 million (previous year: € 41.1 million). The EBIT margin fell by 1.2 percentage points to 11.9 percent (previous year: 13.1 percent). In addition to shifts in the cargo mix, increased union wage rates and the expansion of operations in rail transport also had an adverse effect.

Real Estate subgroup: performance January – June 2024

Despite the weak market environment, HHLA’s properties in the Speicherstadt historical warehouse district and the fish market area of Hamburg maintained their stable trend, with occupancy almost full in the first half of 2024.

Revenue fell slightly by 1.8 percent in the reporting period to € 23.0 million (previous year: € 23.4 million). This was attributable to declining earnings in the fish market area as a consequence of the demolition of cold-storage and warehouse facilities in preparation for a project. This was not fully offset by revenue growth in the Speicherstadt historical warehouse district.

The cumulative operating result (EBIT) dropped markedly by 27.7 percent to € 7.0 million in the reporting period (previous year: € 9.7 million). Alongside increasing maintenance costs, the decrease was chiefly due to expenses linked to the successful reletting of spaces in the Speicherstadt historical warehouse district. Furthermore, earnings were adversely impacted by costs in connection with project-related preparatory work ahead of construction in the fish market area.

Outlook for the financial year 2024

Within the Port Logistics and Real Estate subgroups, HHLA’s actual economic development in the first half of 2024 was largely in line with the forecast published in the combined management report for 2023, which, at the time of preparing the Annual Report, was subject to considerable uncertainty due to geopolitical tensions, the ongoing war in Ukraine and the effects of the announced changes to the syndicate structures of shipping companies.

In the course of the current financial year, economic development in the main markets of the Port Logistics subgroup has been varied. The moderate increase in handling volume due to the economic situation that was recorded in the first quarter of 2024 waned slightly in the second quarter of this year.

Against this backdrop, a moderate year-on-year increase in container handling is now expected for the Port Logistics subgroup (previously: significant increase). The acquisition of a majority shareholding in Roland Spedition GmbH in the second quarter is having a positive effect on container transport, meaning that a significant increase in container transport is now anticipated (previously: moderate increase).

For the Port Logistics subgroup, a significant year-on-year increase in revenue is expected (previously: moderate increase). On the one hand, this development is attributable to the acquisition of a majority shareholding in Roland Spedition GmbH and, on the other, to higher earnings on account of temporarily longer container dwell times at the Hamburg terminals. In the Container segment, the forecast of a significant increase in revenue remains unchanged, whereas a significant increase (previously: moderate increase) is now expected for the Intermodal segment due to the aforementioned majority shareholding.

The operating result (EBIT) is still expected to be within a range of € 70 million to € 100 million. Within this range, a strong increase is expected for the Container segment (previously: strong decrease) due to a higher earnings level, the effects from the remeasurement of the useful economic life of certain assets and a partial reversal of the restructuring provision. A strong increase is still expected for the Intermodal segment.

For the Real Estate subgroup, earnings are expected to remain at the previous year’s level (previously: significant increase).

In total, a significant increase (previously: moderate increase) in revenue is forecast at Group level. The operating result (EBIT) is still expected to be within a range between € 85 million and € 115 million.

Capital expenditure at Group level is expected to be at the lower end of the range of € 400 million to € 450 million. With anticipated investments of € 360 million to € 410 million, the Port Logistics subgroup will account for the majority of this expenditure.

Medium-term Group Performance

The challenging underlying conditions, especially the ongoing war in Ukraine, the crises in the Middle East and the current economic weakness and market changes, are also resulting in a change in the time frame of the Group’s medium-term ambitions for 2025, as presented in 2021. In addition to EBIT of approx. € 400 million for the 2025 financial year, the forecast included in particular total capital expenditure of € 1.6 billion for the period from 2021 to 2025.

The Group continues to target an earnings potential of € 400 million in the medium term. In view of the discrepancy between the planned and actual external conditions, as well as delays to planned asset additions, however, this EBIT potential is now not expected to be achieved before the 2027 financial year.

The Half-year Financial Report is available at:

report.hhla.de/half-year-financial-report-2024

Download image

Container handling at Metrans terminal in Budapest

Share this page on